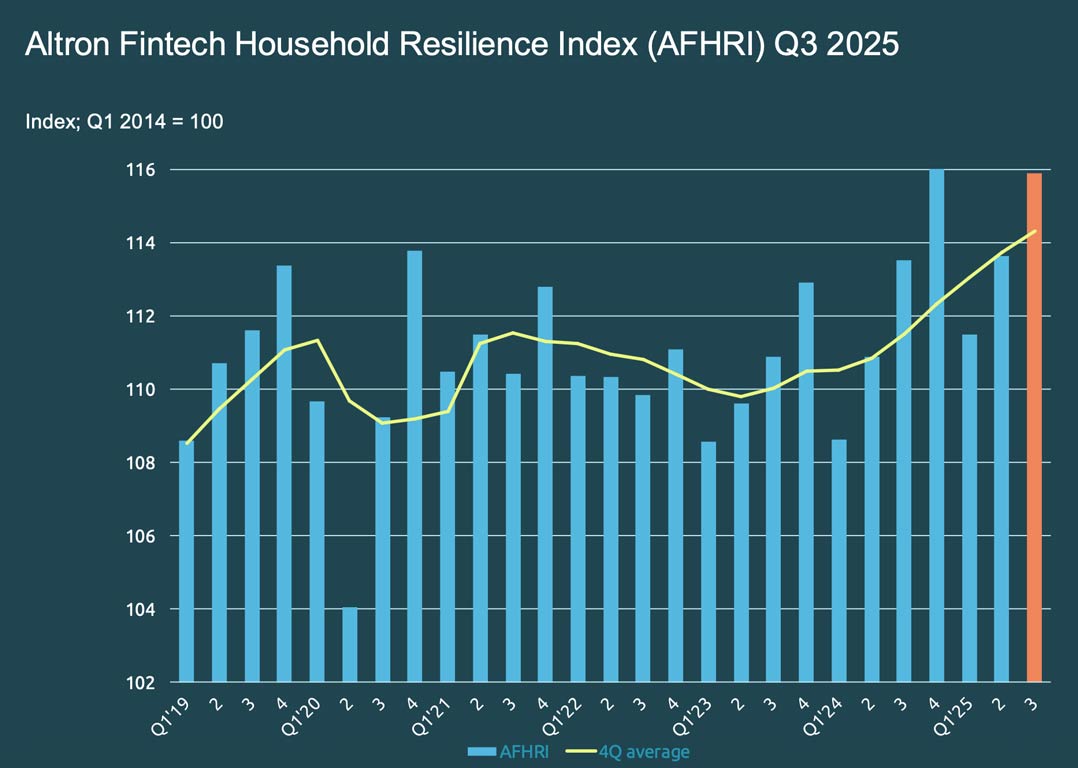

The results of the Altron FinTech Household Resilience Index (AFHRI) for the third quarter of 2025, released on Thursday, show that South African households experienced welcome — though still modest — relief during 2025.

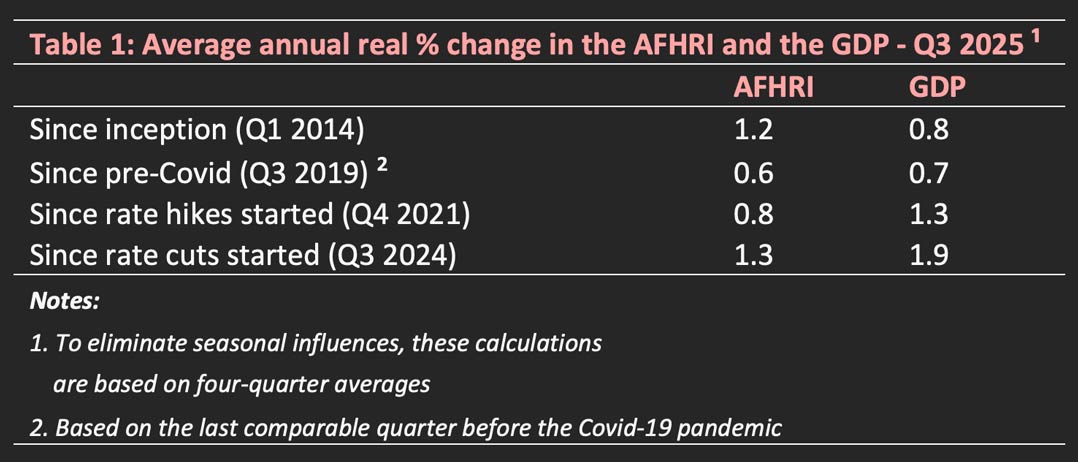

While the AFHRI recorded a healthy year-on-year improvement of 2.1% (largely in line with GDP growth rate), the average annual rise in household financial resilience since the interest rate hiking cycle began remains below 1%.

This implies a negative figure in per capita terms, and points to a continued deterioration in the financial position of South African households. Even so, the slight decline in the prime lending rate supported a gradual recovery in the AFHRI (see figure 1). The results again raise the question of why the prime rate increased from 7% in November 2021 to 11.75% in May 2023 despite the absence of demand -driven inflation – effectively raising the cost of credit by 68%.

Long-term analysis trend

Compared to the last pre-pandemic quarter (Q3, 2019), real household resilience has increased by only 6%/year – slightly below the average annual real GDP growth rate of 0.7% over the same period. Since the AFHRI index launched in 2014, the AFHRI has grown 1.2%/year on average, marginally outperforming GDP. However, households have fared worse than the broader economy since interest rates began rising in 2021, as shown in table 1. Lower rates continue to have a clear positive impact on both the AFHRI and GDP performance.

Impact of pension fund withdrawals

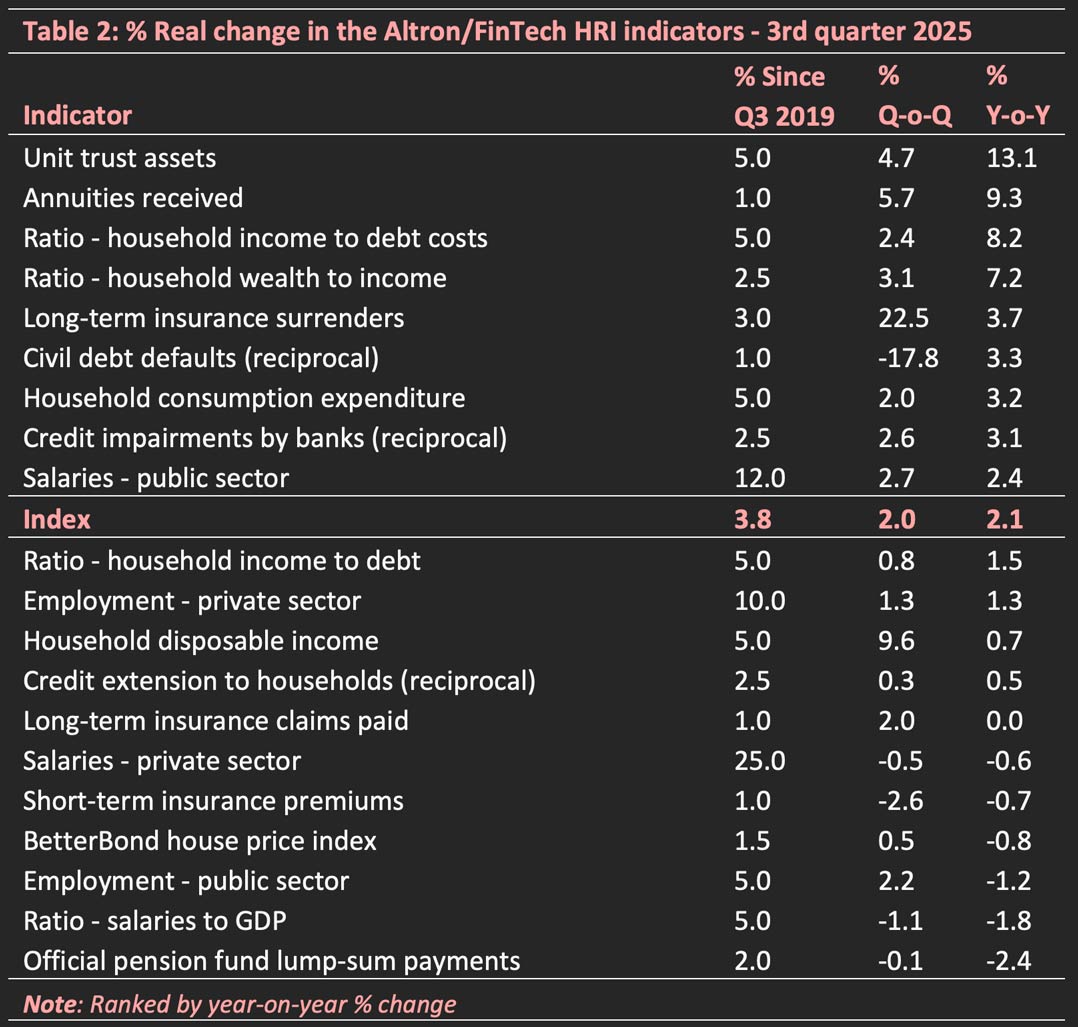

The introduction of the “two-pot” system in September 2024, which allows early access to a portion of a person’s retirements savings, has had a material influence on several AFHRI indicators especially annuity receipts and insurance policy surrenders. In Q3 2025, annuities rose 9.3% year on year and long-term policy surrenders surged 22.5% quarter on quarter, abnormally high movements relative to historical norms prior to the two-pot system.

Between July and September 2025, long-term insurance surrenders totalled R95.3 billion — 42% above the average for the 10 quarters preceding the introduction of the two-pot system. Although the system provides valuable liquidity for households, withdrawals are taxed at an individual’s marginal rate, significantly exceeding the South African Revenue Service’s initial revenue projections.

The effect of lower rates

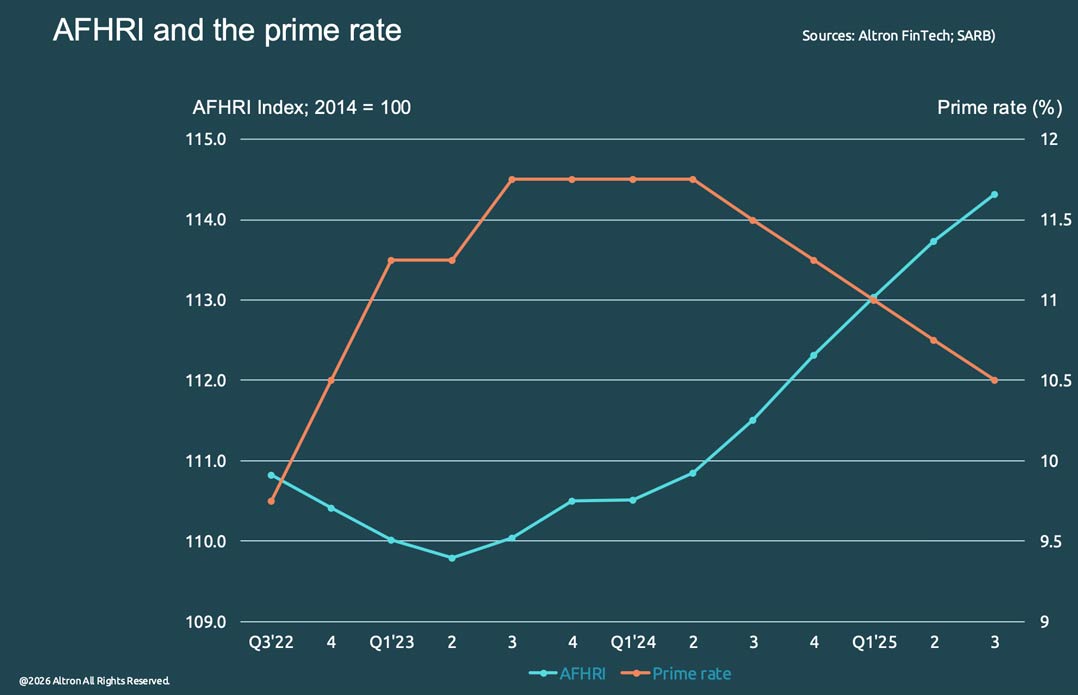

Figure 2 illustrates the strong relationship between interest rates and household resilience. When the prime rate fell 7% in mid-2020, the AFHRI rebounded from a Covid-induced low of 104.1 to 113.8 — a gain of over than 9%. Subsequent rate hikes to 15-year highs weakened household resilience, which only began recovering as rates eased again.

South Africa’s employment landscape remains constrained: formal employment now mirrors the number of unemployed individuals, at just over 11.6 million (including discouraged work-seekers). After a brief improvement in 2021-2022, unemployment rose again as interest rates were increased and GDP growth slowed to below 1% in 2023 and 2024.

With most economists polled by Unisa’s Bureau for Market Research forecasting sub‑2% GDP growth for 2026, more aggressive rate cuts appear essential to reigniting growth and boosting employment.

Q3 2025 AFHRI results

An encouraging feature of the latest AFHRI is the stability that has crept in for the average index value over the past four quarters, which eliminates seasonal influences. The AFHRI’s four‑quarter average reading reached 114.3 — a 0.5% quarter‑on‑quarter rise and a stronger 2.5% improvement year on year. Fourteen of the 20 index indicators improved year-on-year, and 15 strengthened quarter-on-quarter.

Other key trends include:

- Private sector employment improved, though total real salaries edged down slightly.

- Unit trust asset values posted the strongest gains, supported by the JSE All Share Index reaching an all‑time high.

- The income‑to‑debt servicing ratio improved, helped by the rate cut to 10.5% at the end of Q3.

Looking ahead to the fourth-quarter results

The combination of traditional festive-season spending, 13th-cheque payments, and the November rate cut is expected to support further gains in the AFHRI for Q4, 2025. Sustained improvement will, however, depend heavily on job creation.

Johan Gellatly, MD at Altron FinTech, said:

The latest AFHRI results show that although financial pressure on households remains real, the gradual improvement we’re seeing is an encouraging sign that relief is beginning to take hold. Lower interest rates are starting to create space for recovery, and we expect this positive trajectory to strengthen as market conditions stabilise.

At Altron FinTech, we remain committed to equipping financial institutions and businesses with the insights, analytics and technology they need to navigate this period with confidence. Our solutions help organisations anticipate shifts in consumer behaviour, manage risk more effectively and make informed, forward‑looking decisions.

- Read articles by Altron on TechCentral

- This promoted content was paid for by the party concerned